Rare APY of 400%, is TradeXYZ handing out money to oil bulls?

Amid the murky situation of the Iran conflict, the crude oil market has experienced significant volatility.

At the same time, a rare phenomenon occurred in the WTIOIL-USDC crude oil perpetual contract on Trade.xyz: the annualized funding rate remained stable between -300% and -400%. This means that any trader willing to long at this moment would receive daily profits equivalent to 1% of their principal from the short positions.

The market doesn't give away money for free. To understand this abnormal negative rate, we need to start with the basics of futures trading.

Rolling

Crude oil futures are a series of contracts arranged by delivery months. May delivery, June delivery, July delivery, each with its price. As the front month nears expiration, the market transitions from the old contract to the new contract in a process known as rolling.

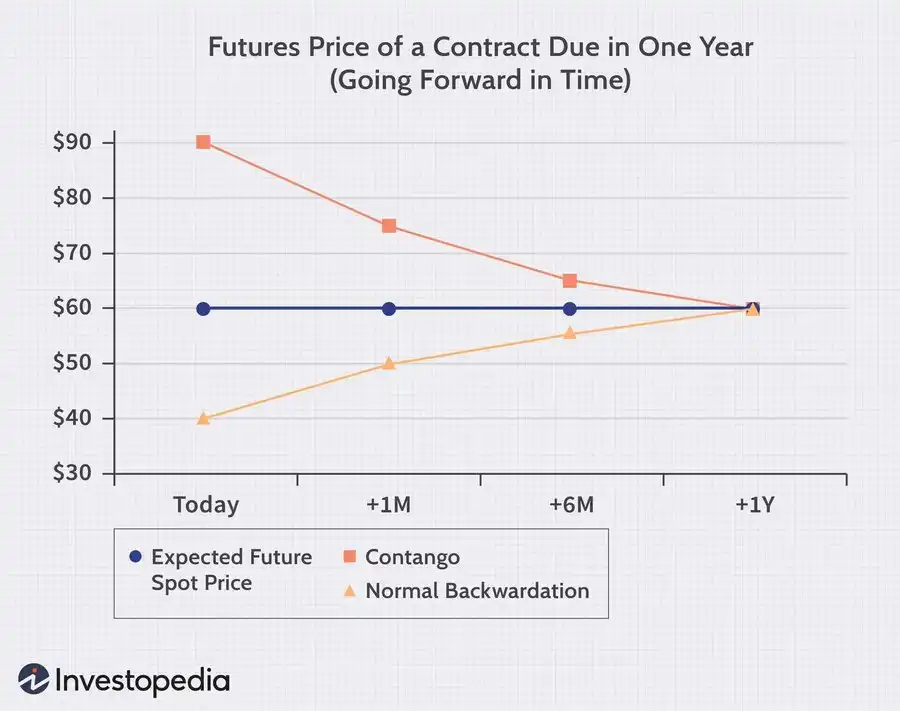

Under normal circumstances, a distant month contract means that oil producers will store the oil for a few more months, incurring additional storage costs. Therefore, the delivery price should be higher. The market refers to the phenomenon where future contracts are more expensive than near-month contracts as Contango, in stark contrast, the situation where near-month contracts are more expensive than distant-month contracts is called backwardation. This usually occurs when there is a current shortage and everyone wants to get the oil now.

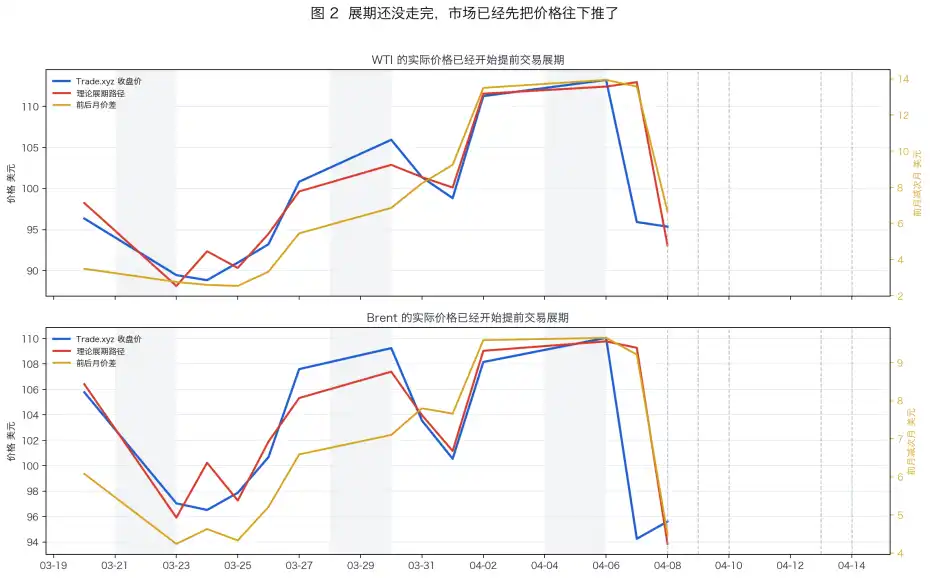

During this Trade.xyz crude oil roll, the crude oil futures market exhibited this structure of near-month prices being higher than distant-month prices.

From late March to early April 2026, the WTI crude oil curve was in an extreme spot price premium. As shown in the above image, the price of the May contract (near-month) consistently remained above the June contract (distant-month), with the spread widening to over $14.

And the WTIOIL-USDC perpetual contract on Trade.xyz had its oracle anchored to this May near-month contract.

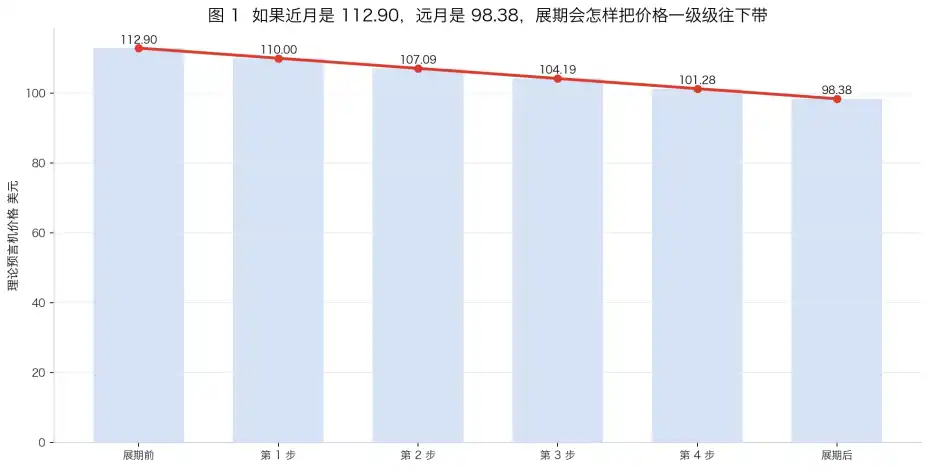

However, we are not going to trade this May contract indefinitely. It must be rolled over to the next June contract. So how is the rolling process executed?

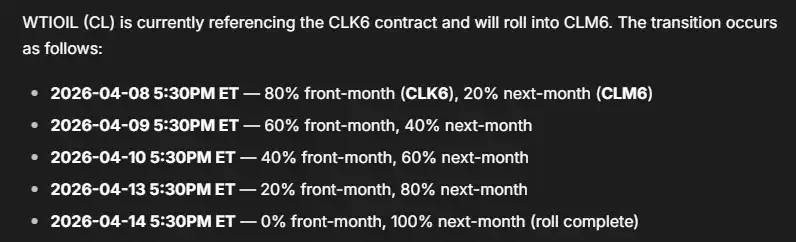

According to the Tradexyz documentation, the oracle will take 5 trading days to gradually shift the price weight from 100% near-month contract to 100% distant-month contract.

In the context of "Spot Price Premium," this means that the oracle price on Tradexyz will drop from the near-month price to the far-month price within 5 trading days.

Market participants familiar with this mechanism have a clear expectation of the post-rollover contract price. Everyone knows it will drop, leading to a rush of short positions. Shorts accumulate, the funding rate turns negative, and shorts start paying longs.

From the perspective of the no-arbitrage principle, this is normal. The price difference between the near month and far month gives shorts a profit. The funding rate then shrinks this profit back. The larger the spread, the higher the negative funding rate the market charges.

Once the negative funding rate reaches a certain point, this seemingly obvious arbitrage will be flattened out again. The shorts' costs will completely cover the profit.

Strategy

How can you make money in such a market scenario? Here are three common strategies.

1. Short Tradexyz's crude oil contract at the current price while going long on the CME far-month contract.

This seemingly risk-neutral strategy can earn a stable spread. However, several factors have not been taken into account.

Assuming a short position on Trade.xyz's WTI contract at $95.352 on April 8, while simultaneously longing the June futures contract at $87.75, each with a $10,000 nominal principal. If both sides eventually converge, theoretically, you can get a price difference of $7.60, equivalent to a profit of about $797. However, the short-term funding rate on April 8 is already at 1.42%. Calculating based on the remaining 6 days until rollover completion, you would need to pay $851 in funding rate. At this point, the net profit is only -$53. This calculation does not yet include transaction fees and slippage.

Abraxas Capital implemented this strategy right after the last rollover on March 19. They held a Brent crude position on tradexyz, accounting for 20% of the market's open interest, and initially gained substantial profits when the funding rate was relatively neutral. However, as more arbitrageurs entered the market, the funding rate has now consumed 80% of their arbitrage profits.

A large position also means they have difficulty exiting and can only passively pay up.

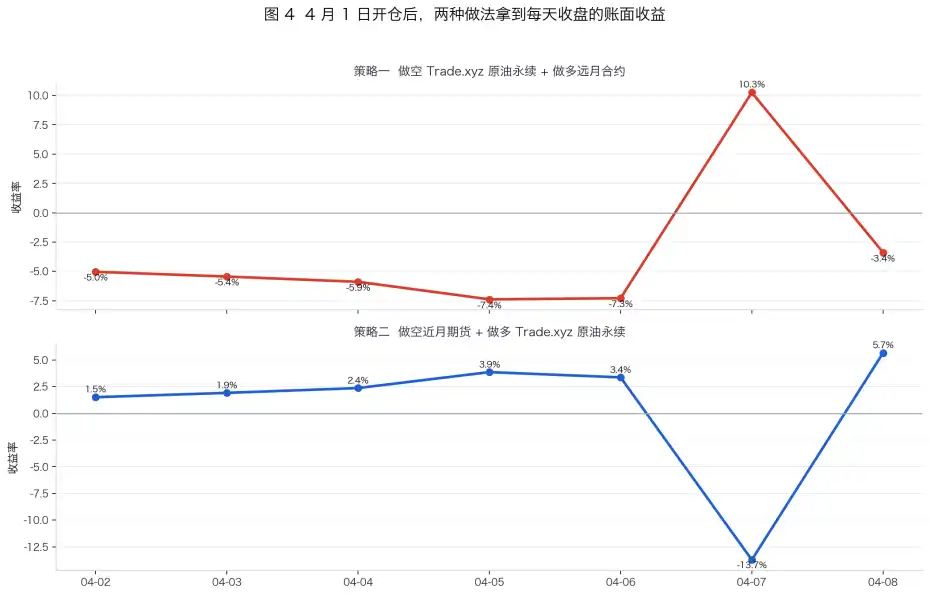

2. Short the far-month futures contract, long the near-month xyz contract, close before the roll

This trade was basically the inverse of Strategy 1, betting on market over-arbitrage. This strategy did pay off after April 1st.

3. Short the xyz contract funding rate on Boros before the roll

Boros is a market specifically developed by the Pendle team for trading rates (fees). In Boros's crude oil contract market, what is traded is the funding rate expectation of the Trade.xyz crude oil contract for the upcoming period. If a user believes the negative funding rate will continue to deepen, they can short the market's funding rate contract.

However, constrained by slippage costs, position limits, trading fees, and very low capital efficiency (supporting only 0.2x leverage), this trade also struggles to achieve the desired high returns.

Conclusion

Trade.xyz and similar RWA trading platforms are forcing a group of "crypto traders" into becoming "futures traders." DeFi players are also starting to learn CME's roll calendar, calculate price spreads between front and back months, and watch the rate curve on Boros to make decisions.

As trading platforms continue to iterate, market participants are also adapting to the new infrastructure.

You may also like

Insiders betting on Musk are reaping "historic returns."

Morning Report | Binance launches DYOR research tool; YZi Labs launches recruitment platform YZi Talent; Vitalik states that the Ethereum Foundation will "downsize" and reduce the amount of ETH sold

Morning News | Michael Saylor stated that this week he bought bonds instead of Bitcoin; StablR was attacked and lost about 2.8 million dollars; the U.S. Congress is pushing the Bitcoin Reserve Act again

SuperEx's Mars exploration dream: Digital currency is the key to unlocking economic exchanges in the interstellar era

Key Takeaways: Full Text of Google Chief Scientist Shanahan's Speech

Agentic Design Patterns: A book that made me rethink "What exactly is an Agent?"

The richest chairman of the Federal Reserve in 112 years has arrived: Kevin Warsh is rewriting the rules

Vitalik talks about the future of the Ethereum Foundation: a smaller, more distinctive, yet more enduring ship

New Types of Information Laundering in Prediction Markets: How Secrets Integrate into Investment Signals

Vitalik emphasized in a post that Ethereum must be "amazing," but the foundation is not the center

DeFi has reached its most dangerous moment: the real vulnerabilities are not in the code

WEEX Bitcoin Pizza Day: Zero Fees, BTC Cashback & 150,000 USDT to Honor Crypto History

a16z: 7 Images to Understand How Tokenization Changes the Nature of Assets

The secret to Hyperliquid's success dismantled from the five-layer financial stack

After Futu Securities was banned, will buying stocks on-chain be the new remedy?

Why Crypto Traders Are Watching Gold and Nasdaq Again in 2026

Why have foreign exchange stablecoins never taken off?